“…these plans have not yet been taxed so they’re sitting ducks for future higher taxes, and that’s exactly what’s going to happen” -Ed Slott, CPA referring to 401k’s and IRA’s.

If you listen to our radio show this Saturday/Sunday at 8am – 9am on News Talk 940 AM then you will hear about taxes in retirement.2 (You see how I slipped that in? Pretty smooth, right?)

In the quote above, the legendary IRA expert and CPA Ed Slott is referring to IRA’s. Congress is grappling with raising taxes now. They seem to be having trouble pulling together any legislation that they all will vote for, but they are trying.

We believe taxes are at the lowest we will ever see right now and they will go up in the future. Many think that they will pay less taxes in retirement because their income will be lower. This isn’t always the case. Let’s walk through some issues.

Social Security is taxed when you make $25,000 – $34,000 for single filers and between $32,000 -$44,000 for married people. Here is where it gets shaky, many think of income as earned income. I punched a time clock put in 8-12 hours and clocked out. Do you think the government would make it that easy when calculating the taxable portion of Social Security? Nay, nay I say.

You must add up ordinary income, IRA income, dividends, capital gains, interest, tax-free interest and ½ of your social security. Many are shocked to see they pay taxes on 50% of their Social Security or 85% if over the range. Tax it all says Uncle Sam!

That is almost everything when adding up your income, almost. Did you notice what is missing? Roth IRA distributions. That is tax free and not (unlike tax-free bond interest) used to calculate the taxable portion of social security.

Having a Roth IRA account can help you control taxes and the tax-rate you pay in retirement. Is that a big deal? I mean does it matter anyway? In our workshops, we show how someone getting ¼ to ½ of their income from a Roth, can reduce taxes by thousands of dollars, every year! (See footnote 1 on how to have the Special Report, “Planning can reduce Tax” sent to you.)1

There is another reason you should really review this issue right now. Taxes are on Sale – only for a limited time! If this is true, we have tax brackets that are going up. The brackets are 0% – 10% – 12% – 22% – 24% – 32% – 35% – 37%

How much will tax rates increase? We are uncertain since our government is a real clown show, (when have they not been a clown show?) but if you are married and make less than $172,750 ($86,375 for a single filer) you will pay 22% tax rate. (12% for amounts under $81,050 if married and $40,525 if single).

We feel strongly that most everyone should look at possibly converting some of your IRA’s or possibly 401k’s into ROTH before years end! But this might not be right for everybody. In the “Special Report How planning can reduce Tax” is a list of 9 reasons a ROTH conversion may not be right for you. So, order a free copy by follow the directions under footnote 1. As always, consult your tax advisor before following advice to be sure it is right for you.

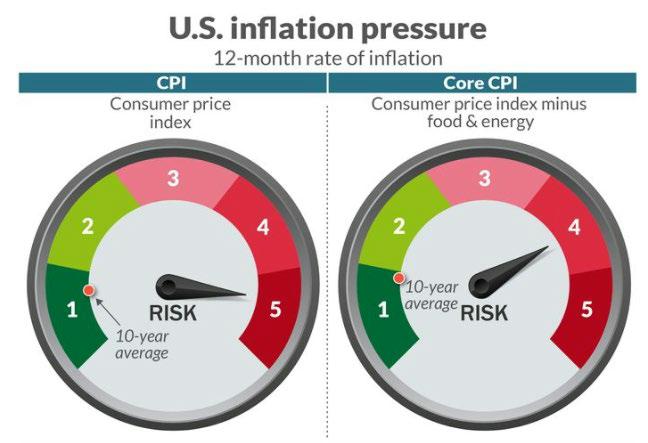

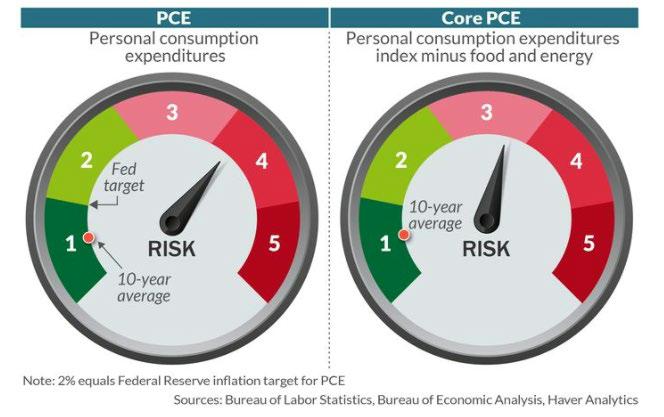

Inflation again!

Headlines we have found

• Professor who called Dow 20,000 says he’s nervous about trends in inflation that could spark a stock-market correction Jeremy Siegel, professor of finance at the University of Pennsylvania’s Wharton School of Business, on Wednesday said that a fresh surge in inflation is making him nervous and warned that accelerating pricing pressures could compel the Federal Reserve to raise interest rates at a faster clip than currently anticipated, which could deliver a correction to equity benchmarks….

“It’s frustrating to see the supply-chain problems not getting better, in fact they are probably getting worse,” Powell said during a virtual forum with other central bank leaders, including those from the European Central Bank.

Source: MarketWatch 9/29/2021

• Inflation rate hits 30-year high, PCE shows, as U.S. confronts major shortages (PCE: personal consumption expenditure) The rate of inflation in the 12 months ended in July edged up to 4.2% from 4% the highest rate since the first Gulf War in 1991

“…senior Fed officials have recently acknowledged that high inflation might persist somewhat longer than they expected.”

Source: MarketWatch Aug. 27, 2021

Social Security Hacks

You lose it unless …

When it comes to Social Security there seems to be a lot of ‘unless’. In my August Social Security Hacks article on Divorced Spouse Benefits, I may have left a little out when I said the following, “Let’s say you decide to remarry. You will no longer be eligible for the divorced spouse benefits.” That was mostly true but there is an unless that I didn’t include. So let me correct it.

Let’s say you decide to remarry. You will no longer be eligible for the divorced spouse benefits unless you marry someone who is receiving Social Security widow(er)’s, mother’s, father’s, childhood disability, divorced spouse’s, or parents benefits.5

As I always tell folks, do not take SSA’s word for anything! They are often wrong. I was only partly wrong and I corrected it. I would like to see Social Security do that!

Sources Citations Bibliography:

⦁ To receive a copy of the special report is entitled, “How planning can reduce tax.” Simply call (888) 814-8559 which is a 24/7 phone line or you can call the office during normal business hours and request a copy.

⦁ For Informational purposes only. Do not rely solely on the Tax and Financial Advice presented here, for it may not be suitable for your individual situation. The preceding is not comprehensive information and needs to be balanced with other factors in your individual financial profile. Consult your legal or tax professional before acting any strategy or recommendation or call us.

⦁ See the SSA Program Operations Manual System. https://secure.ssa.gov/apps10/poms.nsf/lnx/0300202045

Supplemental Disclaimers:

This article is informational only and is not investment advice. This is not an offer to buy, hold, or sell investments like securities or insurance products.

Securities and Investment Advisory Services are offered though Toro Bravo Investment Advisors, LLC. Life Insurance and Annuities sold as an insurance broker are not a fiduciary relationship and are not offered by Toro Bravo Investment Advisors, LLC.

Securities or Insurance are not FDIC/SIPC insured and investments contain risk plus could be subject to loss.

Losses could be short term or permanent. Numbers and figures illustrated are hypothetical in nature and past performance is not a guarantee or indication of future results/performance.

We are not affiliated with the Social Security Administration (SSA), Internal Revenue Service (IRS), or any Governmental Agency.

Do not rely solely on the Legal, Tax, or Financial information presented for it may not be suitable for your individual situation.

Consult your legal, tax, and/or financial professional before acting on any strategy or recommendation (i.e. major changes or before initiating the purchase, hold, or sale of any investment or investment strategy). Every individual’s strategy can differ depending on current circumstances and goals.