“The four most dangerous words in investing are, it’s different this time.” – Sir John Templeton.

“Don’t Fight the Tape, Don’t Fight the Fed!” – Martin Zweig

I get asked all the time, “Where is the market heading?” Truthfully, I don’t know. No one knows. Maybe the Shadow knows? (If you get that then your old.) Here are some economic indicators presented by Herb Morgan:

• October NFIB Small Bus. Optimism Index fell to the lowest point since 2012.

• October Producer Price Index up 8.6% from 1 year ago.

• October Consumer Price index is up 6.2% from 1 year ago.

(Definition of Inflation, too much money chasing too few goods.)

• Weekly Jobless Claims was 267,000 from 271,000 the previous week. California accounted for 21% of the jobless claims. (California has 12% of the US population.)

• 3% (4.4 million) of all workers quit their job in September.

• Earnings 460/500 reporting 374 (81%) were positive and 67 negative with 9.38% of companies showing a upside surprise. (As of 11/15/2021)

At this point, apart from headline risk, we believe the markets are going to trend higher with increasing risks toward a downturn. The overall negative outlook, particularly in the small business optimism index and rampant inflation, is concerning.

Our concern with inflation is if the Federal Reserve has made policy mistakes (counting on inflation being transitory) and now if we are locked into more rampant inflation, the solution is quick rate hikes. We saw these kind of rate increases in the 70’s. The purpose was to induce a recession to end inflation. Yeah, that is a scary little game to play with us.

Currently, inflation should cause companies to see earnings rise. That is good for stocks, but if the consumer begins to spend less and business slow on company asset purchases because of higher prices, then we could slide into a recession. At this point, this is all ‘what if’s’. We believe caution is needed.

So, we are moving to dividend producing stocks, ETFs with dividends, and other income investments. But not bonds! The Fed’s actions continue to influence bond prices and we predict losses in bond portfolios over the next year.

Market based investments that produce dividends could (and likely will) lose value in a market crash. Our prediction is at this point they will out-perform growth over time, going forward. We have started to rebalance to dividend investments. Call us if you have questions on your portfolio.

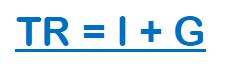

If you reduce investing to the absolute basic formula, it would be:

Total Return = Income + Growth

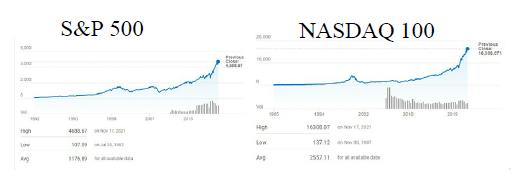

For example, he S&P 500 at its current value kicks off 1.34% of dividend yield. This index is composed of a mixture of mostly growth style investments (or investments that depend on share price appreciation). In the S&P 500 index, there are many stocks that pay dividends. One could argue that the growth portfolio has outperformed the dividend stocks. This would be true and people like us (Financial Advisors) will follow with this statement:

“Past Performance is not a guarantee to future results.”

Many, including Financial Advisors, invest based on past performance. That is dangerous. The past performance has been great in the years before each market crash. (ex. 2000 & 2008) Markets change as does the economy. It is hard to predict the direction the market will take next as Mark Twain once said,

“Prediction is difficult, particularly when it involves the future.”

During market turbulence a portfolio that is kicking out income (dividends) that is either reinvesting while prices are low or (if you are making withdraws) allows you to withdraw income instead of selling shares at depressed prices.

We have seen growth investments massively over perform for the last 10 years. We believe now is the time to shift portfolios away from growth investments, towards income investments. This will not protect you from a market decline, but we expect lower volatility from dividend producing investments going forward.

We do not recommend bonds and bond funds as a class due to interest rate risk and Fed bond buying programs causing issues in the bond markets. If you are pre-retirement or in retirement then you may want to consider principal protected non-stock market investments that have lifetime income protection.

To wrap up, it’s time to move from the G to the I.

Social Security Hacks

Retire Early Pay Dearly by Brian Keith Moon, RSSA

You can retire as soon as 62 years old. But if you continue to work, then you have to cough it back up. What you say? It works like this. First, your benefits will be reduced from what you could have received waiting to Full Retirement Age by 25% and your spouse will see a 32.5% reduction. So, there’s that.

Every dollar you make over $19,560 in 2022, you lose $1 of social security for every $2 you make. Social Security doesn’t ‘do’ partial checks. So, $1 of benefit reduction costs you an entire month of Social Security.

For example, if you make $30,000 you will lose $5,220 in benefits. ($30k – $19560 =$10440/2) But wait! There is more! You will get it back starting at Full Retirement Age and over a 15-year period, provide you don’t switch your benefits. (Claiming Survivor Benefits is a switch.) You need to think carefully before collecting SS and working. It may not be worth it. Call us for help from a Registered Social Security Analyst (RSSA).

Sources Citations Bibliography:

⦁ Herb Morgan is the Sr. Managing Director and Chief Investment Officer of Efficient Market Advisors, See Economic & Market Commentary 11.15.2021

⦁ Headline risk is the possibility that a news story will adversely affect the price of an investment… Headline risk can also impact the performance of a specific sector or the entire stock market. – Investopedia

⦁ China invading Taiwan would be an example of a current headline risk if that was to happen. – Authors

⦁ Federal Reserve Bank

⦁ We manage portfolios on an individual level. We may not apply some of these changes to all clients due to individual suitability or client mandates. Please call to discuss your individual portfolio and the investment strategy we are employing with your accounts.

⦁ PowerShares QQQ Trust Series 1 Stock 10 Year History – Netcials web site

⦁ Call to discuss specific investment options and whether they are in your best interest or meet your financial objectives.

Supplemental Disclaimers:

This article is informational only and is not investment advice. This is not an offer to buy, hold, or sell investments like securities or insurance products.

Securities and Investment Advisory Services are offered though Toro Bravo Investment Advisors, LLC. Life Insurance and Annuities sold as an insurance broker are not a fiduciary relationship and are not offered by Toro Bravo Investment Advisors, LLC.

Securities or Insurance are not FDIC/SIPC insured and investments contain risk plus could be subject to loss.

Losses could be short term or permanent. Numbers and figures illustrated are hypothetical in nature and past performance is not a guarantee or indication of future results/performance.

We are not affiliated with the Social Security Administration (SSA), Internal Revenue Service (IRS), or any Governmental Agency.

Do not rely solely on the Legal, Tax, or Financial information presented for it may not be suitable for your individual situation.

Consult your legal, tax, and/or financial professional before acting on any strategy or recommendation (i.e. major changes or before initiating the purchase, hold, or sale of any investment or investment strategy). Every individual’s strategy can differ depending on current circumstances and goals.