Written by: Brian Keith Moon, RSSA, CF2 and Mubashir Subhani, RICP, CF2

“Well begun is half done.” – Aristotle

“The Bear Stearns Companies, Inc. was a New York City-based global investment bank, securities trading, and brokerage firm that failed in 2008 as part of the global financial crisis and recession, and was subsequently sold to JPMorgan Chase.”

Bear Sterns was founded in 1923. In 2008 the company melted down due to losses in mortgage securities including subprime mortgages.

The federal reserve entered into the crisis in March of 2008 with an ‘emergency loan’ to ‘save’ the company and prevent the contagion from spreading. In the end Bear Sterns was sold to JPMorgan for $10 a share, below the previous high of $133.20 a share. Bear Sterns ended.

Then in September of 2008 Lehman Brothers (formed in 1947, at its peak had a market value of $47 billion dollars and was the 4th largest bank) filed for bankruptcy. This started a global markets meltdown and in October 10, 2008 we saw an intraday low of 7,882 on the Dow Industrial Average down from 11,483 on September 19th and from 14,164 on October 9th 2007. In one year the DJIA3 lost over 44%. It would take 6 years to regain those losses.

You likely heard of the Silicon Valley Bank meltdown. What surprised us was the bank run. What? Is this the 1930’s? That happened to SVB! Then Signature Bank was next to fail. Kevin O’Leary (Shark Tank) called the SVB management team a ‘bunch of idiots’. They shoveled money into technology projects that were extremely risky. They also bought a lot of long dated treasuries before interest rates began to rise. We have been warning or rising rates and the effects on the value of bonds in our educational events since 2019.

When ‘interest rates’ rise the value of existing bonds drop. When depositors ask for their money and if the bank starts selling assets that have lost value, well it doesn’t take long for the bank to run out of money6. It’s like Mary Poppins has come alive. Our government has intervened and we are being told every is ok. “Go back to your homes. We obviously just need more government regulation to fix it.8 The Government that is causing all this. Ironic, isn’t it?”

Here is the short answer. We put too much money into the economy 2020-2022 ($6 trillion) and the fed’s had to increase interest rates to combat inflation. Which caused existing bonds to lose value. Many banks hold these bonds.

We are seeing huge sell offs in bank and financial stocks. We believe that the run is not over. Remember, Bear Sterns was only the beginning in 2008. We also think the Fed will be hard pressed to reverse the rising of rates unless there is a massive recession to combat. Like King Théoden (Lord of the Rings) looking out at a surging hoard of Orcs and Goblins, we have the same worry,

“So it Begins”.

Why? Are you trying to ruin my day? (You ask) No, well maybe, it is our obligation to point out what worries us. One of my clients said to me recently, “you said this would happen last year. It’s like you’re a prophet.” When I showed up in the office in robes, Mandi and Subhani insisted, I change. I am not suggesting you necessarily take drastic action but now is definitely to review your risk & investment strategy.

One of my biggest regrets in life (and I have many) is not taking a more cautious moves for my clients in 2008. History often repeats itself. We have taken a strong cash/CD positions in our managed accounts now. Remember our article last month? Has a bear market trap sprung? January was up 6.18%.10 Like we called it, a bear trap!

Call us to review your retirement and your accounts.

Turmoil for a Swiss Bank

We talked about the problems that maybe starting with banks here in the US, but what about international banking. Remember talk about negative rates in Europe a couple years back?

How do you pay someone to loan them money?

You normally want some kind of interest rate. Negative rates is a brother-in-law deal if I ever heard one. But it was happening in the Eurozone. Those bonds are now worth about half (.53 on the dollar)9 of what they were! With US rates rising, this and other issues have caused Credit Suisse a bank in Switzerland, to be in serious trouble. Let that sink in, Swiss banks are in trouble? To save the bank Swiss authorities developed a plan to give an emergency loan of $54 billion to Credit Suisse. (Sounds like the Bear Sterns story) But that didn’t seem to calm anything so now UBS is going to buy Credit Suisse for $3.25 billion. Credit Suisse stock is currently worth $8.55 billion. Ouch, that is not good. You want to hear the crappy part?

“Switzerland’s executive branch, a seven-member governing body … passed an emergency ordinance allowing the merger to go through without shareholder approval.”

According to ABC news, “Credit Suisse is among the 30 financial institutions known as globally systemically important banks, and authorities worried about the fallout if it were to fail.”

That is nice when the government decides to take your investment away. I think that is not allowed in the US unless a company files for bankruptcy. But in a crisis, anything can happen. Now I repeat for emphasis,

“So it begins.”

Sources Citations Bibliography:

1. Quote from ‘Bear Sterns’ Wikipedia free encyclopedia

2. ‘Lehman Brothers’ Wikipedia the free encyclopedia

3. DJIA -Dow Jones Industrial Average

4. Source Investopedia “The Fall of the Market in the Fall of 2008

5. These numbers excludes dividends and costs.

6. Investopedia “The Inverse Relationship Between Interest Rates and Bond Prices”

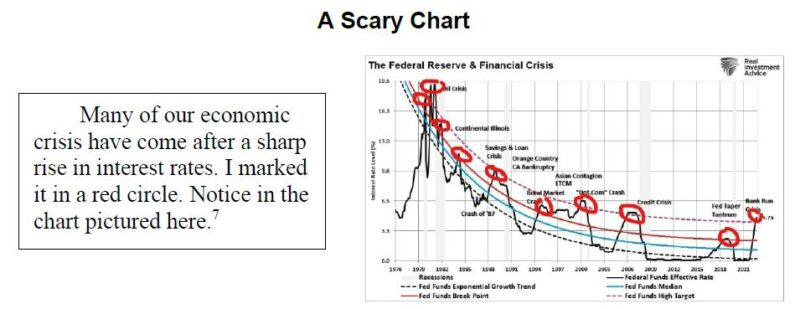

7. Bank Runs. The First Sign the Fed “Broke” Something -Lance Roberts Advisorpedia

8.This is sarcasm. In case you didn’t already know.

9. Reuters Credit Suisse bonds hit

record lows.

10. YCharts.com

Supplemental Disclaimers:

This article is informational only and is not investment advice. This is not an offer to buy, hold, or sell investments like securities or insurance products.

Securities and Investment Advisory Services are offered though Toro Bravo Investment Advisors, LLC. Life Insurance and Annuities sold as an insurance broker are not a fiduciary relationship and are not offered by Toro Bravo Investment Advisors, LLC.

Securities or Insurance are not FDIC/SIPC insured and investments contain risk plus could be subject to loss.

Losses could be short term or permanent. Numbers and figures illustrated are hypothetical in nature and past performance is not a guarantee or indication of future results/performance.

We are not affiliated with the Social Security Administration (SSA), Internal Revenue Service (IRS), or any Governmental Agency.

Do not rely solely on the Legal, Tax, or Financial information presented for it may not be suitable for your individual situation.

Consult your legal, tax, and/or financial professional before acting on any strategy or recommendation (i.e. major changes or before initiating the purchase, hold, or sale of any investment or investment strategy). Every individual’s strategy can differ depending on current circumstances and goals.