There are two ways to make money on your investments. Total Return (TR) comes from either Income (I) from interest and dividends or Growth (G) capital gains/losses or a combination of the two. Income is crucial to those who are in retirement or within 10 years of retirement. Why?

Relying on growth investments for income is dangerous. This is selling shares for income. During down markets, you can seriously erode your retirement savings and risk running out of money before you run out of life. The last two bear markets (first in 2000 and the second in 2008) took 7 and 6 years to recover from. That is a 13-year no-growth market. Since 2009 we have had an upmarket (ending in 2020).

There are serious red flags in our economy. Rampant inflation, rising interest rates, an inverted yield curve, corporate bankruptcies, consumer weakness, and out of control government spending/debt. Consider the inverted yield curve. This is where the short-term bonds and CD rates make more money than the long-term rates. Which is weird because you usually get more interest rate the longer you are willing to commit your funds. Here is the crummy part. After the yield curve inverts it takes 1-3 years before the dreaded recession begins, if at all.

According to Investopedia it says:

“An inverted Treasury yield curve is one of the most reliable leading indicators of a recession.”

We are over 628 days since the yield curve has inverted.2 We see serious problems in the economy but the markets are not showing it. We believe that the historical and unprecedented 6.2 trillion dollars that went into the US economy in 2020-2021 (representing 40% of all the money ever created) has flooded into the markets and is holding them up. Make no mistake, there is no money for nothing. Eventually, the piper has to be paid.

On the positive side interest rates are very attractive. We are recommending a managed bond portfolio for cash flow! (Say that like a late-night DJ) Our grand scheme is to generate a very strong interest yield from bonds and preferred stocks now for cash flow. When the stock market falls, we may recommend moving to dividend stocks (at lower stock prices and a higher yield).

If your account is invested in dividend stocks currently you still have downside share price risk.4 The dividends will cushion your losses in a declining market. The dividends can be paid out in cash for income, saved in a stable investment for emergencies, or reinvested.

“The road goes on forever, and the party never ends.” -Robert Earl King.

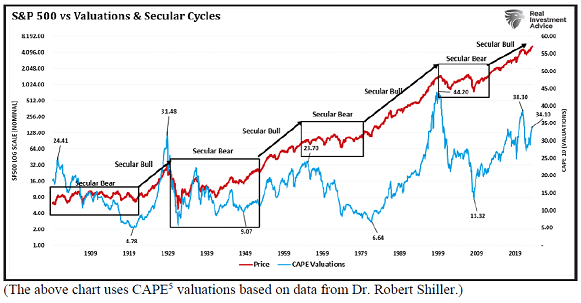

Historically, long periods of ‘secular bear’ markets have followed ‘secular bull’ markets. Falling into the wrong time period can have a detrimental effect on your retirement.

Update: Retire Like You’re on Apollo 13

The book is now slated to drop on Amazon the first week of July. We are planning a book signing at Barnes & Noble and will send out a notice as soon as we nail down a date.

Sources Citations Bibliography:

1. Inverted Yield Curve: Definition, What It Can Tell Investors, and Examples -Investopedia by Daniel Liberto

2. Axios.com

3. The prevailing trend in a “secular bull” market is “bullish” or upward-moving. In a “secular bear,” the market tends to trend sideways with severe drawdowns and sharp rallies. -Seeking Alpha ‘The Next Secular Bear Market May Be Upon Us’ by Lance Roberts

4. If you wish to review a debt securities portfolio please call us.

5. “CAPE ratio is a valuation measure that uses real earnings per share (EPS) over a 10-year period to smooth out fluctuations in corporate profits that occur over different periods of a business cycle. The CAPE ratio, using the acronym for cyclically adjusted price-to-earnings ratio, was popularized by Yale University professor Robert Shiller.” -Investopedia.com

Supplemental Disclaimers:

This article is informational only and is not investment advice. This is not an offer to buy, hold, or sell investments like securities or insurance products.

Securities and Investment Advisory Services are offered though Toro Bravo Investment Advisors, LLC. Life Insurance and Annuities sold as an insurance broker are not a fiduciary relationship and are not offered by Toro Bravo Investment Advisors, LLC.

Securities or Insurance are not FDIC/SIPC insured and investments contain risk plus could be subject to loss. Losses could be short term or permanent.

RSSA – Registered Social Security Analyst. RICP – Retirement Income Certified Professional. CF2 – Certified Financial Fiduciary

Economic and market information has been obtained from published sources. While we believe such sources to be reliable, TBIA does not assume responsibility for the accuracy of such information. Numbers and figures illustrated are hypothetical in nature and past performance is not a guarantee or indication of future results/performance.

We are not affiliated with the Social Security Administration (SSA), Internal Revenue Service (IRS), or any Governmental Agency.

Do not rely solely on the Legal, Tax, or Financial information presented for it may not be suitable for your individual situation.

Consult your legal, tax, and/or financial professional before acting on any strategy or recommendation (i.e. major changes or before initiating the purchase, hold, or sale of any investment or investment strategy). Every individual’s strategy can differ depending on current circumstances and goals.