I admire Elon Musk, but not to the point where I track his plane and post locations on Twitter (Elon shut that site down when he bought the Twitter). It’s admirable how he has turned start-ups with massive risk of failure into raging successes. He has been through the ringer when his companies ran into past recessions. Elon tells how Paypal and Tesla nearly went bankrupt and how SpaceX was out of money. If the 3rd launch had failed, they would have been bankrupt.

Recessions destroy some businesses and damage others for long periods of time, this is known. As Financial Advisors, the common advice we give is, Buy and Hold. The market always comes back from every recession, every time. This is true if you are able to Hold. But what if you are approaching retirement or currently retired? Drawing income or making distributions when retiring violates the ‘hold’ principal.

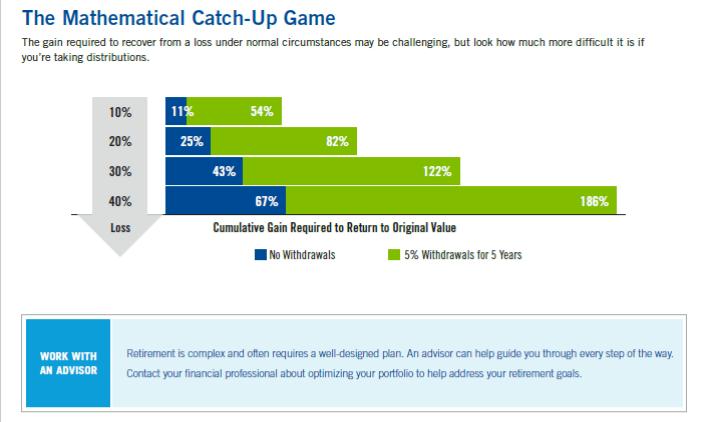

This graphic1 shows the effect of drawing income from your accounts during a downturn.

But what about pre-retirement and post retirement investors? Volatility can have a devastating effect on your retirement. The chart below makes the point.

If you lose 30% and take 5% in annual withdrawals, you would need an average 24.4% return2 to get back to where you were! Even if you have a long investing timeline, this can potentially cause you to run out of money in retirement.

Past downturns have taken 7 and 6 years to recover3. Too many advisors incorrectly treat those near or in retirement as suitable for growth style strategies because they have a 10 year plus investment timeline. They may be encouraged by their firm to keep clients in investments or investment managers that benefit the brokerage firm, or they may be addicted to risky Wall Street gambling. It is hard to tell. Drawing funds from an account during a market drop will erode your retirement as sure as anything. (See graphic above)

Our clients may have noticed we are investing in CDs4 money markets and dividend stocks in our managed accounts. Short term CD rates are quite high so we are taking advantage of this. If the stock markets indeed drop, we can shift to stocks again. We also have a 3rd party manager for bonds. That is an option if you wish to discuss it.

Now back to Elon Musk. According to Shanthi Rexaline at Benzinga, “Musk tweeted on Sunday, adding that a “mild recession is already here.” Furthermore, “It’s not like just the canary in the coal mine (SVB) died, one of the staunchest miners (Credit Suisse) died too & the cemetery is filling up fast!” he wrote. Warning of danger ahead, “Further rate hikes will trigger [a] severe recession. Mark my words,” he tweeted.5 We agree if there is a recession, it’s the Fed’s fault.

CF2 – Certified Financial Fiduciary

Two years ago in May, we completed our course work and testing for the CFF (Certified Financial Fiduciary) designation. Recently the CFF became accredited by ANSI National Accreditation Board. This is apparently a big thing. What is a Certified Financial Fiduciary you ask, and why is it important to you?

A CFF designee has completed a comprehensive course on Fiduciary responsibilities and agree to uphold the NACFF (National Association of Certified Financial Fiduciaries) code of conduct. (Go to FINRA.ORG Professional Designations CFF)

Many writers of articles tell you to only work with a Fiduciary. The reasoning is a fiduciary must always put your interests first and clear or disclose all conflicts.

Here is the rub. There are many instances where a product (fixed annuities as an example) might be in the best interest of the client. However, the advisor that manages an account for a fee often can’t offer products that might be in your best interest, or they attach fees to a product that you could have gotten without additional costs. Many annuities don’t offer the same features when bought through a ‘fee only’ advisor.

The SEC (that regulates the markets and securities industry) understands this problem (I am surprised!). There have been calls to expand the definition of a legal Fiduciary to virtually everyone. Some of those pushing for this have a real goal of ending commission-based products they don’t like. The SEC instead changed the suitability rules that Broker/Dealers used to work under. These rules were very liberal.

The new rules are called Best Interest. These rules are not perfect, but they mandate commission-based advisors to disclose all matters important to the transaction. Part of the Best Interest regulations require a form CRS (Customer Relationship Summary) to be provided to customers detailing services, fees, conflicts of Interests, compensation, legal or disciplinary history, and on. This form is similar to the ADV given by an IAR Fiduciary, which contains like information. This form is intended to encourage you to ask questions and do your comparisons and make you aware of all considerations.

All this information you are being given is intended to ensure that the Financial Advisor is operating in your best interest. The same as a Fiduciary advisor would. The goal is to protect the customer. If you know anything about bureaucracy, it’s that it isn’t perfect. The Best Interest rule is an attempt put commission-based transactions under the same obligations that a Fiduciary has. This makes a competitive and free market in financial products. Paying an ongoing fee is not always in your best interest. I believe the Best Interest rule was a smart compromise to requiring Fiduciary for all.

As for us, we are Wealth Managers. We manage accounts for a fee as a Fiduciary, but we also sell insurance products as brokers and also sell securities as brokers, where we are commission based, which we do under the best interest rules. Our multiple lines of businesses allow us not to be pigeon-holed into offerings that don’t fit your situation. Instead, we independently offer what works best for you.

Telling you all this is complex and we probably left something out. The reason we earned of CFF designation is it combines our values of putting you first with a committed planning process across all types of businesses and relationships.

The CF2 Code of Conduct requires loyalty, good faith, and good care, to educate, to use a holistic approach, provide comparisons, have professional practice management, and protect confidentiality with full disclosure.

By using a planning/education process (which is different from a sales process), we focus on what your financial, income and risk needs are first, before making an investment recommendation and educate you on your options rather than to sell you. When you invest, we provide you the advice that is in your best interest whether we are legal fiduciaries or not. This is our commitment to you and your family.

Sources Citations Bibliography:

1. Source: The Real Cost of Volatility -Franklin Templeton 02/11/2020

2. We consider a 24.4% 5-year average return unlikely and an unrealistic goal.

3. S&P 500 drop in 2000 recovered it’s full price in 2007 & the 2008 recovered in 2013. This is price only, dividends and costs are not included.

4. CD – Certificate of Deposit that carries FDIC insurance up to $250,000 per individual. Only CDs are insured by FDIC. This does not extend to the other investments in the account that carry market risks and are subject to loss, including money market investments.

5. Source: MSN.com Benzinga 5/1/2023 by Shanthi Rexaline

6. Annuities we are referring to are Fixed and Fixed Index.

7. U.S. Securities and Exchange Commission

8. Conflicts of Interests where other people, considerations or financial interest can affect the advice given to you causing biased advice.

9. Insurance Brokers can represent multiple insurance companies.

10. Toro Bravo Investment Advisors, LLC is a state of Texas Registered Investment Advisor. Toro Bravo only provides advice and management under a fee arraignment. Broker activities either Insurance or Securities are offered by the advisor separate from Toro Bravo and not as a fiduciary. See our ADV for full disclosures.

11. Source: National CF2

Supplemental Disclaimers:

This article is informational only and is not investment advice. This is not an offer to buy, hold, or sell investments like securities or insurance products.

Securities and Investment Advisory Services are offered though Toro Bravo Investment Advisors, LLC. Life Insurance and Annuities sold as an insurance broker are not a fiduciary relationship and are not offered by Toro Bravo Investment Advisors, LLC.

Securities or Insurance are not FDIC/SIPC insured and investments contain risk plus could be subject to loss.

Losses could be short term or permanent. Numbers and figures illustrated are hypothetical in nature and past performance is not a guarantee or indication of future results/performance.

We are not affiliated with the Social Security Administration (SSA), Internal Revenue Service (IRS), or any Governmental Agency.

Do not rely solely on the Legal, Tax, or Financial information presented for it may not be suitable for your individual situation.

Consult your legal, tax, and/or financial professional before acting on any strategy or recommendation (i.e. major changes or before initiating the purchase, hold, or sale of any investment or investment strategy). Every individual’s strategy can differ depending on current circumstances and goals.