“Be Fearful when others are greedy and greedy when others are fearful.” -Warren Buffett Legendary Investor

Last month’s lead article was, “When is it time to cash out?” We focused on the 3 investing principals: Diversify, Buy & Hold, & Have a Plan. We are in unprecedented times as far as the markets are concerned. We shut down the US economy last year and saw a remarkable -31.4% decrease in 2nd quarter GDP.1 To keep things in perspective, consider the GDP for the financial crisis of 08-09; GDP for 2008, 2009, & 2020

All of 2008 = –2.01%, All of 2009 = -2.4%, & All of 2020 = -3.5%

These numbers resulted in a -38.49% decline in the S&P 500 index2 in 2008. So, what was the damage to the market in 2020 with the worse GDP decline ever?3 The S&P 500 was up +17.88%4 What? How is this possible?

“Don’t Fight the Fed.” – Marty Zweig American stock investor

One thing to remember about the markets is, they are not always controlled by corporate earnings. They can be a function of supply and demand. There are three things that are happening that is affecting the economy and stock markets.

1. The Fed’s are buying bonds. This reduces supply of bonds for investors and increases cash in the economy. (The Federal Reserve balance sheet has $8.3 trillion today from $1.2 trillion 200710)

2. Interest rates continue to be 0 -.25%.

3. Stimulus programs have dumped about $4.5 trillion into the economy.

40% of all the money ever created, has been printed in the last year.

That is staggering when you think about it. When do we pay this back? Right now, no one cares. The markets are punch drunk on all the money. S&P 500 companies are profitable. Trailing PE Ratio6 is 27.29 for an average valuation.

Is that right? So, the market is not OVER valued here? That is tricky and depends on who you talk to. The forward PE based on the next 12 months is 23.26. The money in the economy is helping corporations which results in a higher stock market.

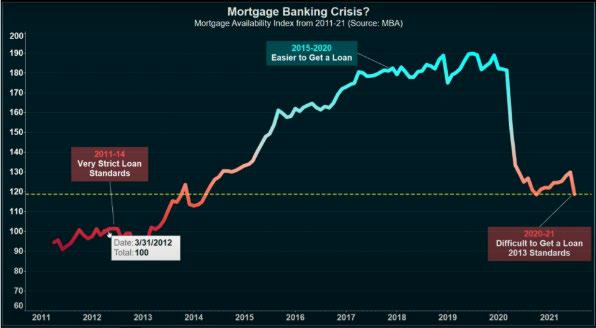

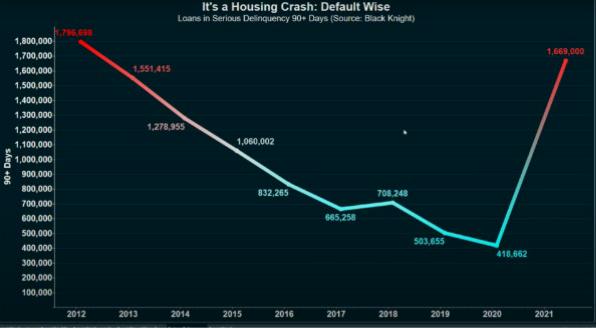

One area we are concerned about is foreclosure risk and bank lending standards tightening. The chart’s below are concerning.

Why are banks tightening when they have so much cash available? There is a wave of foreclosures coming. That is why the government is attempting to issue mortgage moratoriums through the CDC8, which SCOTUS9 shot down.

Inflation is a major problem and the Federal Reserve continues to maintain that inflation is short term. Other economic news looks good and unemployment has improved dramatically and now stands at 5.4%.

If we are seeing a bubble forming, then we are likely early. We expect some market volatility over foreclosures, which is one of reasons politicians are eager to complete the infrastructure bill.

Trying to predict when the bubble will burst is tricky. If you are close to or in retirement, it may be time to reduce your equity positions. We have a number of options that can help secure your income and lower risk in your invested assets.

Stock market recoveries can take years to happen and can derail your retirement plans. It is better to make plans in favorable times.

“Be scared when everyone else is greedy.”

Samson the Toro Bravo Therapy Dog

I recently moved my Rotten Lab, Samson (Rottweiler – Labrador mix), dog into my office space. He is getting old (10 years), has hip dysplasia (common in his breed) and needed to be inside. We posted his picture on Facebook. The DOG got over 600 likes and comments. More than any other of our posts! Our Facebook page has great articles on personal finance, but most everyone really like seeing Samson.

Social Security Hacks

Divorce Spouse Benefits

To claim Social Security Benefits on a divorced spouse earnings record, the following conditions must be met:

• You must have been married 10 years

• Your spouse must qualify for benefits (must be at least 62 years old).

• You have to be divorced 2 years

You may claim a Social Security benefit that is 100% of your benefit or 50% of your divorced spouse’s social security benefit (Not both).

Let’s say you decide to remarry. You will no longer be eligible for the divorced spouse benefits. After 1 year, you could collect 50% on your new ‘love of your life’s’ earnings record. (Provided he/she is collecting SS benefits.)

But wait, his social security check is going to be less than yours! What can you do? Divorce him (or her), cite tiny social security on the divorce forms and you will become re-entitled for the previous spouse. Whew! Disaster averted.

Finally, let us say your ex-spouse dies. If you remarry before age 60, you lose survivor benefits (unless that marriage ends) then you can become re-entitled. After 60, you can get re-married without forfeiting Survivor Benefits. Why? I guess social security figures you are older, wiser and need the money.

Sources Citations Bibliography:

⦁ BEA.GOV. GDP -Gross Domestic Product is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. -Investopedia

⦁ macrotrends.net S&P 500 historical annual returns

⦁ Forbes.Com GDP Plung 32.9%. Here’s why it matters.

⦁ With dividends reinvested. DQY DJ Website.

⦁ GSI Exchange Website

⦁ PE Ratio is the ratio for valuing a company that measures its current share price relative to its per-share earnings. – Investopedia

⦁ Stock Market PE from Ratio.com

⦁ CDC – Center for Disease Control

⦁ SCOTUS – Supreme Court of the United States

⦁ PGPF.org

⦁ Trading Economics

⦁ Samson the dog is not registered to give financial advice. He does reduce stress of the TBIA team and whines when someone doesn’t pet him.

⦁ We do not recommend getting divorced in order to increase Social Security. Don’t give ‘Tiny Social Security’ as a reason on divorce forms. That was a joke.

⦁ We do not recommend killing your ex-spouse as Social Security benefits will not payout. God doesn’t like it, neither does law enforcement (again a joke)!

Supplemental Disclaimers:

This article is informational only and is not investment advice. This is not an offer to buy, hold, or sell investments like securities or insurance products.

Securities and Investment Advisory Services are offered though Toro Bravo Investment Advisors, LLC. Life Insurance and Annuities sold as an insurance broker are not a fiduciary relationship and are not offered by Toro Bravo Investment Advisors, LLC.

Securities or Insurance are not FDIC/SIPC insured and investments contain risk plus could be subject to loss.

Losses could be short term or permanent. Numbers and figures illustrated are hypothetical in nature and past performance is not a guarantee or indication of future results/performance.

We are not affiliated with the Social Security Administration (SSA), Internal Revenue Service (IRS), or any Governmental Agency.

Do not rely solely on the Legal, Tax, or Financial information presented for it may not be suitable for your individual situation.

Consult your legal, tax, and/or financial professional before acting on any strategy or recommendation (i.e. major changes or before initiating the purchase, hold, or sale of any investment or investment strategy). Every individual’s strategy can differ depending on current circumstances and goals.