“All capital investments inherently suffer the risk of permanent capital loss. As an investor, it is your job to differentiate between market volatility and a permanent capital loss.” – Naved Abdali Financial Author

If you have saved and invested for any amount of time, you know and understand Volatility! You understand that markets and investments will lose value, sometimes a lot of value. The mantra repeated by all investment advisors, stockbrokers and planners of all brands is: Buy and Hold for Long Term and Diversify. Just like Warren Buffett the legendary investor did.

The markets have always comeback from every decline, every time. This is generally good for accumulators. Accumulators don’t require withdrawals from their accounts. They can wait for investments to recover.

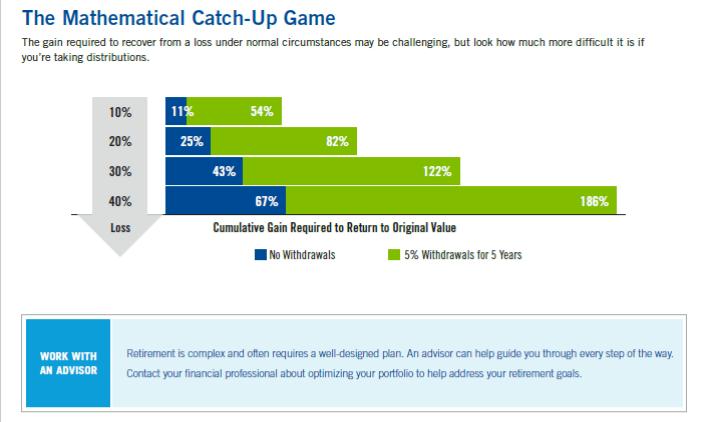

But what about pre-retirement and post retirement investors? Volatility can have a devastating effect on your retirement. The chart below makes the point.

If you are an accumulator and the market loses 10%, you only need a little over 11% to get back to where you were. If you lose 20%, then you need a 25% increase to be back. According to CNBC, a 30% decline over 14 months takes 2 years to recover. If you are adding this up that’s over 3 years.

Notice, how much you need if you are taking 5% withdraws from your account. A -10% drop will need a +54% cumulative return (over 5 years). A -20% decline will need +82% and you can see how bad it gets -30% or -40%!

Many investors have had success in accumulation, but the math changes in retirement. The last couple declines had a shorter than usual recovery.

Are you prepared to forgo withdrawals for 3 years or more to prevent depleting your retirement and running out of money?

How do you solve your problem? Call us to set a complimentary appointment.

Headlines We Found

Bank of America Warns Earnings Growth Could be “Vaporized”

Bank of America just put out a big warning that advisors need to pay attention to. The bank is warning that earnings growth could get “vaporized” across a couple of sectors. The reason why is tax hikes. BofA’s Savita Subramanian posits that in a scenario where taxes rise to 25% next year (from 21% this year), 5% would be wiped off earnings growth, a huge margin in a year that is already set up to see some cooling after the red hot earnings growth of 2021. Source: Finsum 09/03/2021

• UBS Sends a Stark Warning to Equity Investors

UBS just put out a very interesting warning to a large segment of the equity market. As part of their overall market outlook update, UBS explained their view on earnings and the direction of the S&P 500. There are two very notable points they made. Firstly, and most importantly, they reminded investors to stop fretting over valuations. In their words “While valuations are higher than average, we remind investors that valuations have no correlation with market returns over time horizons less than three years … And valuations typically don’t contract meaningfully unless investors are concerned about a sharp growth slowdown or a policy error by central banks. And secondly, they think the S&P 500 will rise 11.5% by the end of 2022. Source: Finsum 08/25/2021

• Bond Legend Warns of Huge Correction

“When you say bond legend, only one name likely comes to mind (let’s leave Gundlach out of this for a minute): Bill Gross. And old Bill always has an opinion, and this week it is a very strong one: “bonds are trash”. Bill says that bonds are now in the investment garbage can because Fed tapering in the first half of 2022 will likely cause a rise in Treasury yields from 1.3% now to 2% next year, causing an overall loss of around 3% over the next 12 months. According to Gross, “Cash has been trash for a long time but there are now new contenders for the investment garbage can. Intermediate to long-term bond funds are in that trash receptacle for sure.” – Source: Finsum 09/03/2021

Social Security Hacks

Increasing Your Social Security Check after 70

Does working after age 70 benefit or hurt your social security check? First, there is no penalty for working after full retirement age of 66/67. Your benefits stop being adjusted for wage growth after age 60. Your AIME is based on your best 35 years of earnings over your life. This number is not frozen when you start collecting SS. After age 60, your earnings could add new top numbers to your 35 earnings years. “Social Security will automatically recalculate your AIME and all the retirement benefits tied to it.”

If your income is higher than your past earnings, your check (with other benefits, like your spouse’s if based on your SS) will increase! If your income is lower than your top 35 years then there is no effect. You will continue to pay social security taxes, which stinks.

Sources Citations Bibliography:

⦁ Past Performance is not a Guarantee to Future results. Buy and Hold does not protect from bankruptcy or failure of an investment.

⦁ Source: The Real Cost of Volatility -Franklin Templeton 02/11/2020

⦁ Source: cnbc.com 02/27/2020 Heres How Long Stock Market Corrections Last and how bad they can get.

⦁ AIME- Average Indexed Monthly Earnings adjust past earnings to account for inflation.

⦁ “because of wage inflation the federal government indexes wages so that $35,648.55 earned in year 2004 is exactly the same as $23,753.53 earned in 1994. Those two figures came from the yearly list of National Average Wage indexing series. This series gross up earlier years wages so that all years earnings up to age 60 are put on equal footing.” -Wikipedia

⦁ Source: 2016 Edition Get what’s yours, Social Security. –Kotlikoff, Moeller, and Solman

Supplemental Disclaimers:

This article is informational only and is not investment advice. This is not an offer to buy, hold, or sell investments like securities or insurance products.

Securities and Investment Advisory Services are offered though Toro Bravo Investment Advisors, LLC. Life Insurance and Annuities sold as an insurance broker are not a fiduciary relationship and are not offered by Toro Bravo Investment Advisors, LLC.

Securities or Insurance are not FDIC/SIPC insured and investments contain risk plus could be subject to loss.

Losses could be short term or permanent. Numbers and figures illustrated are hypothetical in nature and past performance is not a guarantee or indication of future results/performance.

We are not affiliated with the Social Security Administration (SSA), Internal Revenue Service (IRS), or any Governmental Agency.

Do not rely solely on the Legal, Tax, or Financial information presented for it may not be suitable for your individual situation.

Consult your legal, tax, and/or financial professional before acting on any strategy or recommendation (i.e. major changes or before initiating the purchase, hold, or sale of any investment or investment strategy). Every individual’s strategy can differ depending on current circumstances and goals.